Assets & Elbows: Lithium Americas In The Lithium Triangle

On a whim I wrote this article late in 2021 and submitted to Seeking Alpha, which they promptly rejected three times. So fuck them, but I'm posting it here because - what do you know - its now relevant with Ganfeng's purchase of Pluspetrol's Pozuelos-Pastos project for a whopping $962M. Some of the info and maybe even my own opinions may be outdated, but I'm not going to rewrite it.

- - - - -

Primary tickers: $LAC $MLNLF $AMRZF Secondary tickers: $ALB $SQM $GNENF $LTHM

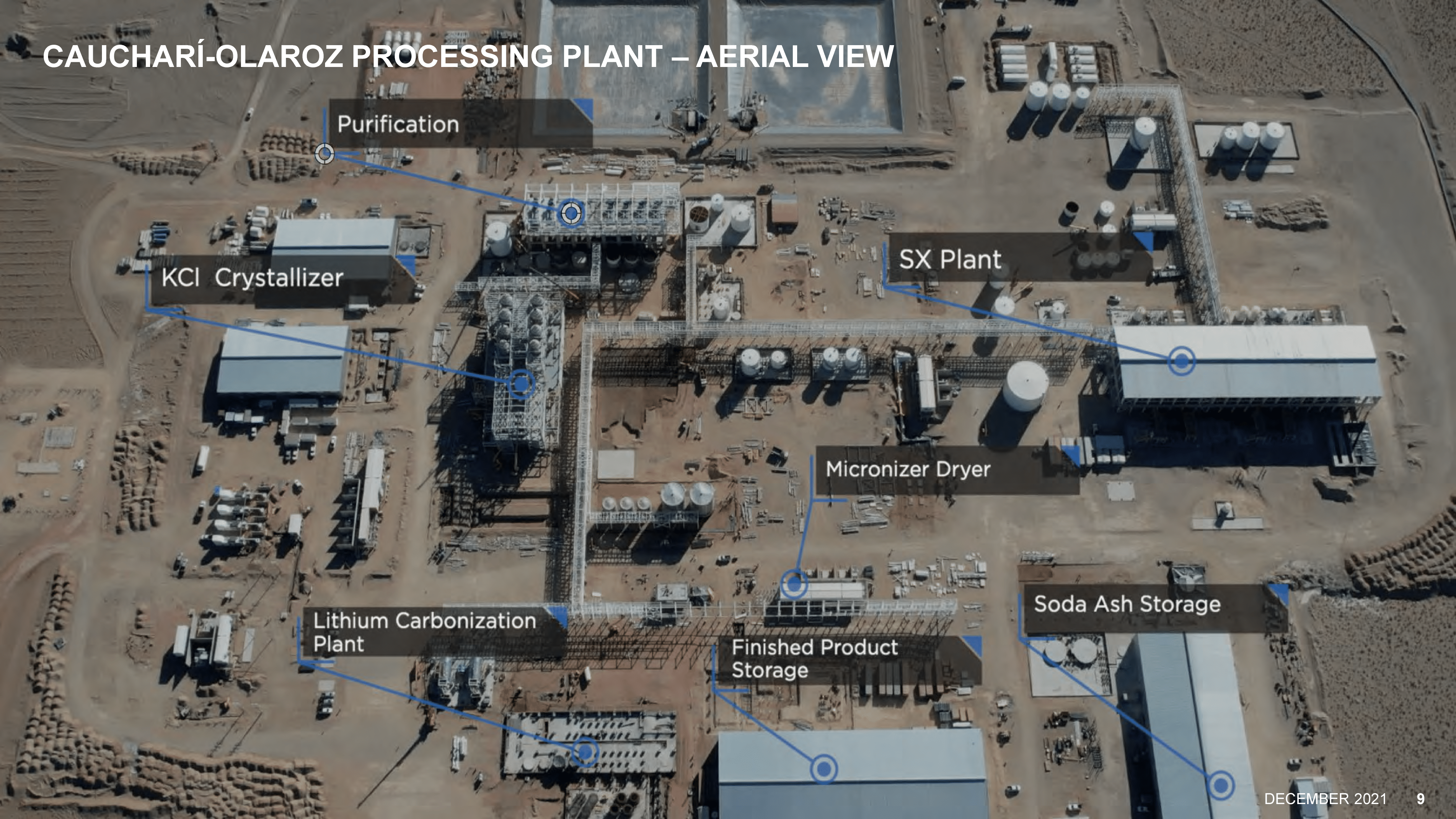

Lithium Americas ($LAC) has been raising capital, making investments, and generating excitement about the company’s position for growth. They are carving out footholds in the Lithium Triangle while inching closer to revenue from their premiere Argentinian lithium operation at Cauchari-Olaroz in 2022.

Months ago the focus was on Lithium Americas’ Thacker Pass mine in Nevada and the legal triumphs and tribulations there. In the lull leading up to the expected court ruling there, early this year, the spotlight has moved from Thacker Pass below the equator to the Lithium Triangle.

Unmatched among lithium juniors in their ability to raise capital, the company is beginning to reveal how they intend to use it. We’ll take a look at some key developments, both new and old in their corner of the triangle and piece together a picture of how Lithium Americas may look in South America once the lithium sector matures.

The Assets

Two junior miners have drawn Lithium Americas’ gaze recently: Millennial Lithium ($MLNLF) and Arena Minerals ($AMRZF), both have lithium brine projects in Argentina. Millennial’s flagship project is Pastos Grandes which sits only about 60mi (100km) south of Lithium Americas’ and Ganfeng’s (GNENF) joint venture at Cauchari-Olaroz. Arena’s main project is Antofalla located 185mi (300km) to the southwest, but they also hold some peripheral land at Pastos Grandes.

Source: data by USGS, map by author

Millennial Pioneers Pastos

Millennial Lithium has been developing the area since 2016 and has completed a fair amount of exploration, culminating in a 2019 feasibility study. A significant portion of this salar (salt flat) is also controlled by Litica (a Pluspetrol subsidiary), and the minor component by Arena Minerals.

To weigh Millennial’s project, we can start with their 2019 feasibility study. They define a 1.7M tonne LCE mineral reserve out of a 4.1M tonne LCE resource. The mine life is 40 years and its productivity is largely pond-limited, though the well network is also designed pretty tightly. Millennial estimates a 61% Li recovery overall, and a base-case NPV-8 just north of $1.0B after tax.

It’s no surprise they received competitive bids, eventually selling to Lithium Americas in a $400M deal. This project is well advanced and stands on its own, but is close enough to Lithium Americas Cauchari-Olaroz to also share company resources. However you feel about the $400M price tag, the move proves that Lithium Americas will not be content with just a single joint venture project in Argentina; they will be expanding.

Arena Minerals In View

Arena Minerals has a peripheral claim at Pastos Grandes. On its face, this wouldn't seem to add much to the broader Pastos project. If Lithium Americas (with Millennial claims) also acquired Arena’s land, it could open up some additional pond area, and the combined project’s economics should improve somewhat with a resource expansion. This is not where all of their value lies however.

Arena also has two land positions in the Salar de Antofalla which, the company claims, hosts a unique lithium brine and is anticipated to be a sizable deposit in and of itself. The brine chemistry is not in the public eye yet and to date there have not been any feasibility studies released here so its difficult to even venture a guess as to the value of Arena’s holdings in Antofalla.

Lithium giant Albemarle ($ALB) rather boldly claimed in 2016 when they acquired their own Antofalla position that this area would become known as the largest deposit in the lithium triangle.

Allkem ($OROCF) (formerly Orocobre) also has a large 32,000 acre (13,000 ha) land position adjacent to Albemarle here. Clearly, these heavyweights have a keen interest in this highly prospective basin and the sky just might be the limit.

The Elbows

With few exceptions, the largest and best deposits in the lithium triangle were divided and conquered years ago and the potential for new discoveries is becoming more and more limited. Most, if not all of those original projects are either expanding, producing, or under construction. They all sit on large reserves and with lithium’s price trend have plenty of room for expansion.

{kind=link}

{kind=link}

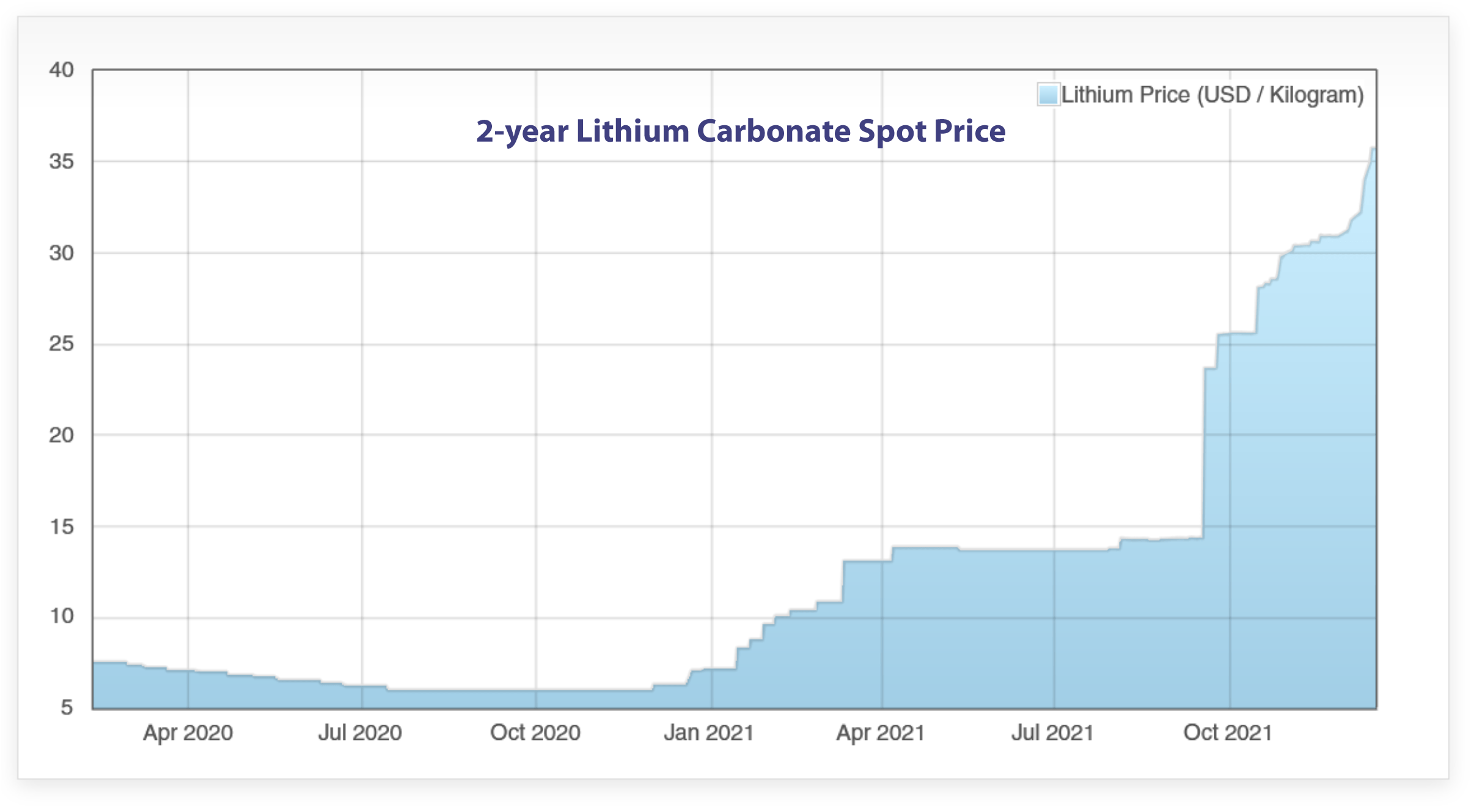

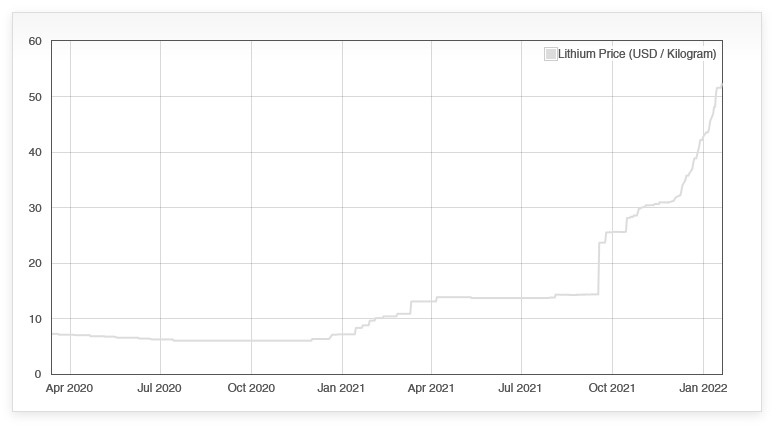

Source: https://www.dailymetalprice.com

Nevertheless, they don’t run the show completely. Value is still being created elsewhere by quantifying known deposits, consolidating property, and optimizing operations.

Some deposits are divided up so badly that an individual project struggles to justify the capital spend necessary to reach production. Their options are then pretty limited as to how they can advance. The most likely outcome is capitulation: they sell, they joint-venture, or they wait.The following is an example of a tough land position owned by Lithium South at Livent's Hombre Muerto salar. The thing that stands out is that they own five isolated claims. Its a question of footprint. Where can you put a well field and tap into the aquifer? Where can you fit your evaporation ponds? Whats the terrain like? Can you run a pipeline across someone else's claim if they also control the surface rights?

Source: NRG Preliminary Economic Assessment

These more moderate scope projects currently in development face a critical dilemma: do their economics justify building a standalone operation fully equipped with all the bells and whistles and a shiny new lithium carbonate plant, or do they benefit from taking an intermediate “cog in the wheel” role in a larger process chain?

Consider the well established oil industry in the United States. If you were to develop a well field to extract crude oil in west Texas, you are not going to also build a refinery there and sell gasoline. Your operation would sell into a crude oil pipeline downstream 500mi to a refining hub somewhere like Houston, TX. Granted, this analogy takes us only so far and there are significant differences between the lithium and petroleum sectors.

It is interesting though that every brine project bases their value on standalone operations, but it is unlikely that this will remain possible for every operation if existing suppliers and infrastructure will be pushed beyond capacity in the near to mid term.

Reagent Squeeze

Any traditional brine operation consumes large amounts of chemical reagents, namely lime and soda ash. Lime is primarily consumed in the concentrate ponds to help to remove impurities, while soda ash is the essential reagent in a lithium carbonate plant. All lithium brine producers, even direct-lithium-extraction (DLE) operations need these reagents.

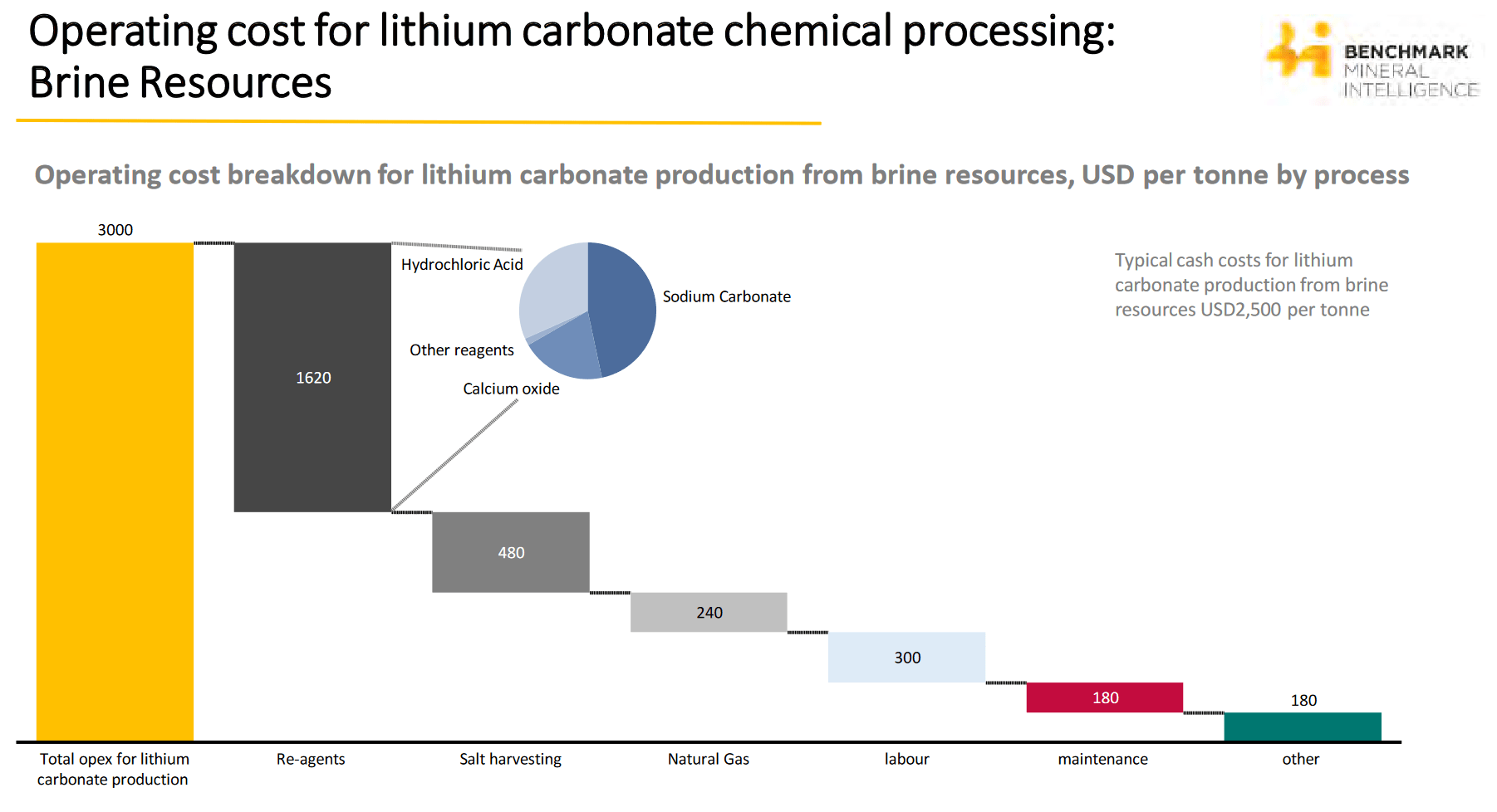

Nearly every feasibility study from the lithium triangle makes the same recommendation: secure a reagent supply. The reason is obvious when you consider the importance of process continuity and potential savings. Reagents make up typically around 50% of total operating costs, of which lime and soda ash compose the majority.

{kind=link}

Source: Benchmark Mineral Intelligence, Millennial Lithium Pastos Grandes 2019 Feasibility Study (available on SEDAR)

There is one soda ash producer in Argentina, reportedly at capacity, so new supply currently comes in from port. There are a few lime suppliers but their operations need expansion.

Lithium Americas’ Cauchari-Olaroz feasibility study mentions a smallish reagent lime supplier within 90mi (150km) and a backup within 750mi (1200km). The latter is a fair distance and would be the equivalent of the Thacker Pass Mine in northern Nevada trucking in their lime from Albuquerque, NM.

Lime supply: We recommend that efforts to firm up lime supply source be pursued. The area producer will require support for increasing production capacity as other local producers are depending on the same source. [Lithium Americas] intends to obtain lime from this source and discussions for providing additional support are underway.

- Lithium Americas Cauchari-Olaroz 2020 Updated Feasibility Study

This all speaks to a tightening reagent supply in the triangle and the impetus for major producers to secure these vital consumables for their own operations and future expansions.

Gas Pains

Lithium producers also require electrical and thermal energy. In more remote areas both are often provided by natural gas. Argentina produces a large amount of natural gas, but the supply is bottle-necked by existing pipelines feeding these remote areas. Every new project and project expansion in the triangle will be looking at securing a gas allocation, if they haven’t already acquired one.

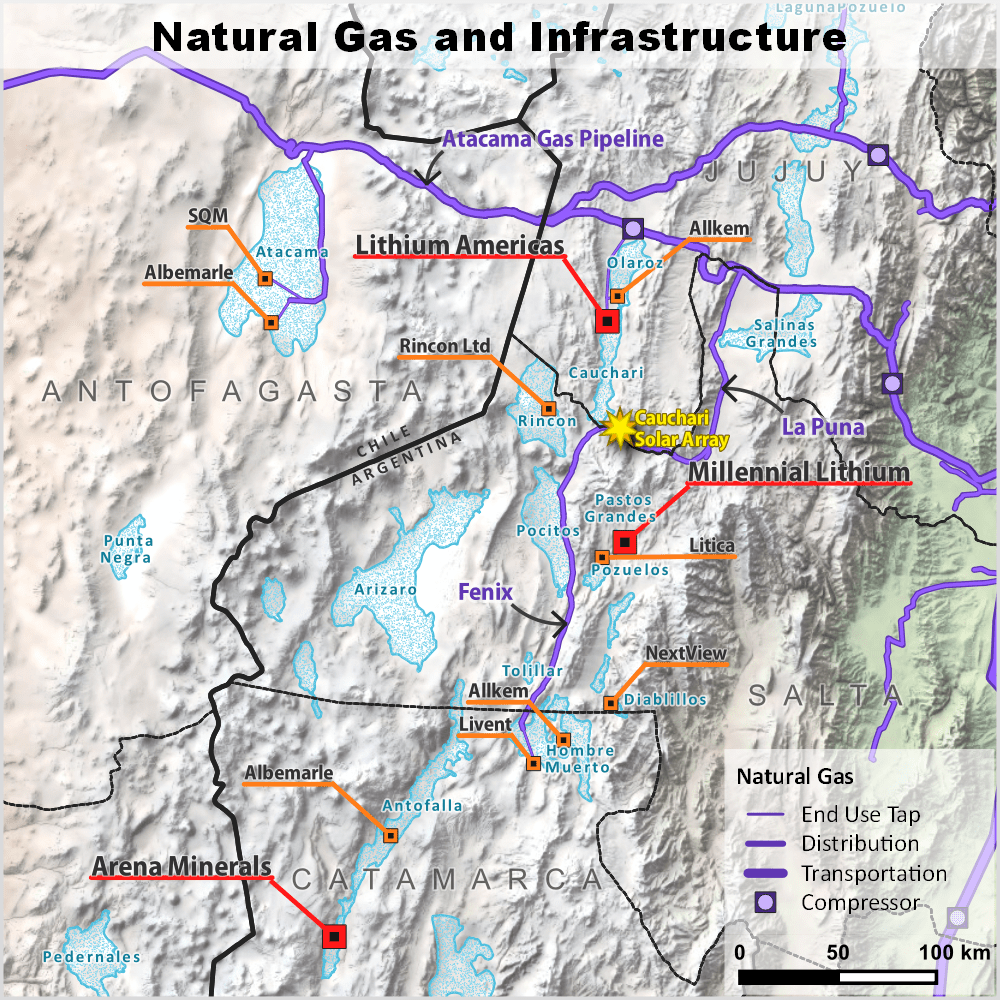

Lithium Americas’ Cauchari-Olaroz project required constructing a 33mi (52km) natural gas pipeline with capacity to support 50kt LCE annual production. While that is enough for their initial operation it does not cover their planned expansion, so even as an operating producer they still need to secure additional capacity.

{kind=link}

Source: data by Argentina ENARGAS, map by author

Millennial’s Pastos Grandes project would require construction of a 23mi (37km) natural gas pipeline to their site. The company states that they have secured gas capacity on the La Puna pipeline branch, but less than what they would require for full production. That doesn’t provide for much flexibility and leaves no room for future expansion. It's worth noting that Lithium Americas has presumably acquired their gas rights in the buyout.

Not every project in development can be supplied by existing infrastructure and capacity expansions will take time to develop in concert with these projects. It’s also a sure bet that current producers are locking down supply lines for their planned expansions.

Arena Minerals’ Secret Sauce

The longtime producers in the triangle, namely the OGs in the Atacama salar, operate at a very low cost not only because their brines are rich and the evaporation rate is high, but because they are able to produce some of their own reagent in-house from brine.

The basic idea for Arena Minerals is that their Antofalla brines offer a complementary chemistry that, when mixed with other brines in the region, eliminates the need for a significant amount of costly reagent.

Arena Minerals’ Executive Chairman and chemical engineer Eduardo Morales used this technique when he pioneered the Lithium Triangle with Rockwood Lithium Latin America (now Albemarle) before lithium ion batteries were mass produced.

Albemarle and SQM ($SQM) currently use a similar process in their Atacama operations in Chile. It just so happens that both chemistries are available within the same deposit (conveniently for them).

This has been Arena’s angle and competitive edge since Mr. Morales was brought on board in 2018, right before they acquired their Antofalla property. It also explains the intense interest Lithium Americas and their partner Ganfeng have given them over the past year.

Our objective is to ultimately own and operate several high-quality assets and supply lithium chloride to a centralized chemical plant. We are convinced this is the future of the brine lithium industry, allowing assets to be developed without incurring excessive capital costs while reducing the technical risk of having to build and operate a chemical plant.

- Arena Minerals Press Release Feb 4, 2021

What does it all mean?

Existing triangle producers Albemarle, Allkem, Livent, and SQM have their foothold. If you're investing in smaller junior projects, eventually competition is going to catch up to you. Not all will make it to production. The senior miners here know what's up, and they aren't giving away any layup opportunities to the many smaller projects, but Lithium Americas and Arena may just send those juniors a bounce pass.

Let's get right down to it. Lithium Americas wants in on Arena Minerals because of their Antofalla brine and proprietary process to produce a lithium-bearing reagent concentrate which can supply an array of low cost satellite projects producing lithium chloride which then feed a centralized lithium processing plant.

{kind=link}

Source: Lithium Americas December 2021 Corporate Presentation

This is the endgame as I see it. Not every project needs a lithium carbonate plant; not all of them want one. There are huge cost savings and risk reductions to be had by producing a moveable, intermediate product like 25% lithium chloride; particularly if there is a high capacity local reagent supplier and a low capital option for easy off-take that can get you there. Battery-grade purity issues could also be benefited by feed-blending and more robust purification circuits.

Maybe a centralized plant is developed by Lithium Americas and Ganfeng in another JV, maybe one of the longtime producers steps up, or a new player comes to town.

Someone, at some point will have every reason to build a very large lithium refinery for the lithium triangle. When that happens it will fundamentally improve the economics of new brine operations in the area. It's the path of least resistance to maximum production and efficiency from the region.

Valuation

When Lithium Americas produces a couple kilotons of lithium carbonate this year they will officially step onto a very small stage with few other brine producers. If they can capitalize on the moment and keep moving aggressively, they have a chance to quickly outgrow the more sluggish senior producers with this strategy.

From a growth point of view, they have plans to expand production at Cauchari-Olaroz. Pastos Grandes is ready to receive capital and move into construction, and Antofalla is ripe for drilling. From an operational perspective, their costs would be cut handsomely by developing a lithium-bearing reagent supply and additional resource sharing.

At worst, Lithium Americas is lining up a pipeline of organic project growth in the triangle which they can foster with their incoming revenue and operational presence. At best, they dominate this arena by scooping up strategic assets, partnering into upstream supply lines and downstream processing, cementing their role as a gatekeeper to the triangle while lowering the price of entry to the numerous other upstarts coming online.